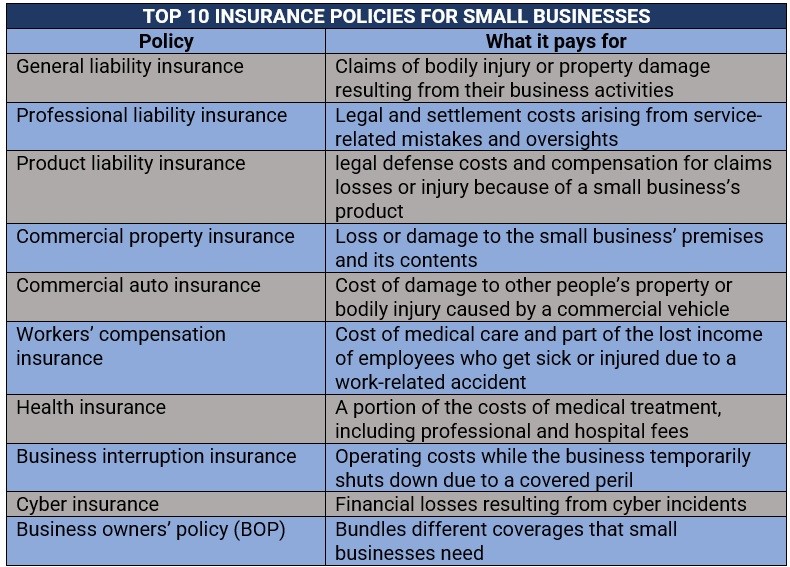

Top 5 Insurance Policies Every Small Business Owner Should Consider

As a small business owner, protecting your investment is crucial. One way to ensure your business's longevity is by securing the right insurance policies. Here are the Top 5 Insurance Policies you should consider:

- General Liability Insurance: This policy covers claims of bodily injury, property damage, and personal injury. It provides essential protection against lawsuits that could otherwise jeopardize your business.

- Professional Liability Insurance: Also known as errors and omissions insurance, this is vital for service-based businesses. It protects against claims of negligence or failure to deliver services.

- Property Insurance: This policy covers damage to your business property, including buildings and equipment, caused by events such as fire, theft, or vandalism.

- Workers' Compensation Insurance: Required in most states, this provides coverage for employees who are injured on the job, ensuring they receive medical benefits and lost wages.

- Business Interruption Insurance: This type of policy helps replace lost income if your business is temporarily unable to operate due to a disaster or other unforeseen events.

How to Assess Your Insurance Needs as a Small Business Owner

As a small business owner, assessing your insurance needs is crucial for protecting your investment and ensuring long-term success. Start by identifying your unique risks and vulnerabilities, which can vary widely based on your industry, business size, and location. Make a list of assets that need coverage, including property, equipment, and inventory, and consider potential liabilities, such as customer injuries or data breaches. Analyzing these factors will help you understand the types of insurance necessary to safeguard your business.

Once you have a clear picture of your risks, you can explore the various types of insurance that may be applicable. Common options include general liability insurance, which protects against third-party claims, property insurance for physical assets, and workers' compensation insurance to cover employee injuries. Additionally, consider specialized policies like professional liability insurance if your business provides services that could lead to client grievances. Regularly revisiting your insurance needs is essential as your business evolves, so set a schedule to reassess these requirements, ensuring adequate protection against emerging risks.

What Are Common Insurance Mistakes Small Businesses Make and How to Avoid Them?

Small businesses often make several common insurance mistakes that can lead to significant financial repercussions. One frequent error is underestimating coverage needs; business owners might opt for lower premiums by minimizing their policy limits, leaving them vulnerable to hefty out-of-pocket expenses in the event of a claim. Additionally, failing to regularly review and update insurance policies can lead to gaps in coverage, especially as the business grows or changes. To avoid these pitfalls, small business owners should perform an annual review of their insurance needs, ensuring that their coverage aligns with the current state of their business.

Another common mistake is not understanding the specifics of their policies. Many small business owners assume they are adequately covered without reading the fine print, which can result in unpleasant surprises when filing a claim. It's crucial to take the time to read and comprehend policy details, including exclusions and limitations. Business owners should also consult with a knowledgeable insurance agent who can help them navigate the complexities of commercial insurance. By educating themselves about their coverage, small business owners can better protect their assets and avoid costly mistakes.